The purpose of this CXTech Week 14 2021 newsletter is to highlight, with commentary, some of the news stories in CXTech this week. What is CXTech? The C stands for Connectivity, Communications, Collaboration, Conversation, Customer; X for Experience because that’s what matters; and Tech because the focus is enablers.

You can sign up here to receive the CXTech News and Analysis by email. Please forward this on if you think someone should join the list. And please let me know any CXTech news I should include.

Covered this week:

- Get Ready for more SMS SPAM, as Facebook wins in the Supreme Court

- Perpetually Surprised

- TADSummit Asia 2021 Update

- Well done to the hSenid Mobile team powering Commercial Bank’s WhatsApp interface

- Will private wireless kill network slicing before it even gets started? No.

- People, Gossip, and Frivolous Stuff

- Amazon’s Private Labels – its complex, but it’s more or less a monopoly

- Blacc Spot Media, Inc. is celebrating its 10th year anniversary today!

Get Ready for more SMS SPAM, as Facebook wins in the Supreme Court

In CXTech Week 12 2021 News and Analysis I mentioned the Supreme Court case between Facebook and Noah Duguid, and the likely outcome being in favor of Facebook given the pro-Facebook forces spent a collective $184.7 million on federal lobbying across all issues in 2020, employing a collective 689 unique lobbyists.

The court concluded that an illegal auto-dialing system “must use a random or sequential number generator,” and this definition “excludes equipment like Facebook’s login notification system, which does not use such technology.” As mentioned CXTech Week 12, lawyers and politicians are the reason the US has failed to tackle spam robocalling.

Perpetually Surprised

A nice Twitter thread made into a blog from Erlend Prestgard of Working Group Two. Which reminded me of the discussion Erlend and I had last year at TADSummit EMEA / Americas 2020, shown below.

For many of the individuals within the telcos, they are not surprised. Rather the organization does not have an adequate public response to anticipated external threats, other than BAU (Business As Usual). It’s the classic curse of legacy and the focus on next quarter’s results.

Back in 2017 Patrice Crutel gave a great presentation on the role Cap Gemini plays in helping enterprises take control not only of their services thanks to IP; but also their networks, e.g. private LTE. 5G SA is the current fashionable technology to talk about, but Patrice showed 4 years ago how it is possible.

Interestingly, I’m seeing many companies with significant cloud computing resources beyond Google, Amazon and Microsoft, e.g. Dell, getting serious about private enterprise 5G mobile networks.

A key quote from Erlend is “A very few will take on the ambition to themselves become tech companies.” That is now perceived as a large and risky leap in business model. Back in the ’90s, outsourcing technology made sense when only a few companies in the world were capable of telecoms research and innovation in DSL, FTTH, VoD, IMS, etc. In today’s software defined world, being a tech company it not such a high barrier. Simwood is a great example.

The barrier is more cultural than access to skills (generally web / internet) or technology (see Working Group Two). I discussed this last year in my response to the ““Accelerating Innovation in the Telecommunications Arena” paper. To quote Peter Drucker, “Culture eats strategy for breakfast.” It is the telco’s culture that blocks innovation. I can share tens of stories of telcos failures to adopt innovations from start-ups that went on be successful on the internet, here’s an example from Khairil’s (Group Chief Marketing & Operations Officer at Axiata Group) TADSummit 2014 keynote.

There are successes, check out my weblog on ‘Keep an Eye on Malaysia‘. Innovative services can incubate within a telco taking advantage of favorable initial conditions, but there comes a time to set them free to move beyond the telco and achieve national or regional dominance. Telcos are operating companies, not technology companies. Incubate and spin-out is likely the best recipe.

- Telco – operating company. Takes someone’s technology, e.g. mobile network technology, and given a state-granted oligopoly, operates the asset relatively efficiently to distribute SIM / phones to customers for a well understood service everyone needs.

- Innovative Service – technology company. Building out their platform technology, in control of the roadmap and customer experience. Able to continuously hone the customer experience and craft the platform to chase new business and find local recipes that work.

TADSummit Asia 2021 Update

Bogdan is back with a session on how OpenSIPS will help you compete over the coming decade.

OpenSIPS. Or How One Open Source Software Project Disrupts all Telecom Customs!

Bogdan-Andrei Iancu, Founder and Developer at OpenSIPS Project

The Open Source Software paradigm is revolutionizing the telecoms world; in terms of IPR, licensing, and market value. Witness the explosion of new enterprise communication service providers such as RingCentral, 8X8, Talkdesk, Twilio, and many more; all using open source software.

To remain competitive in a fast changing telecoms market requires a change in ideology. Open Source Software helps realize the benefits of that change in ideology.

OpenSIPS, an open source VoIP software, is accelerating this ideological change. It is one software able to deliver almost the full spectrum of VoIP solutions: from SBCs, SoftSwitches to Virtual PBXes.

Come learn how OpenSIPS will help you compete over the coming decade.

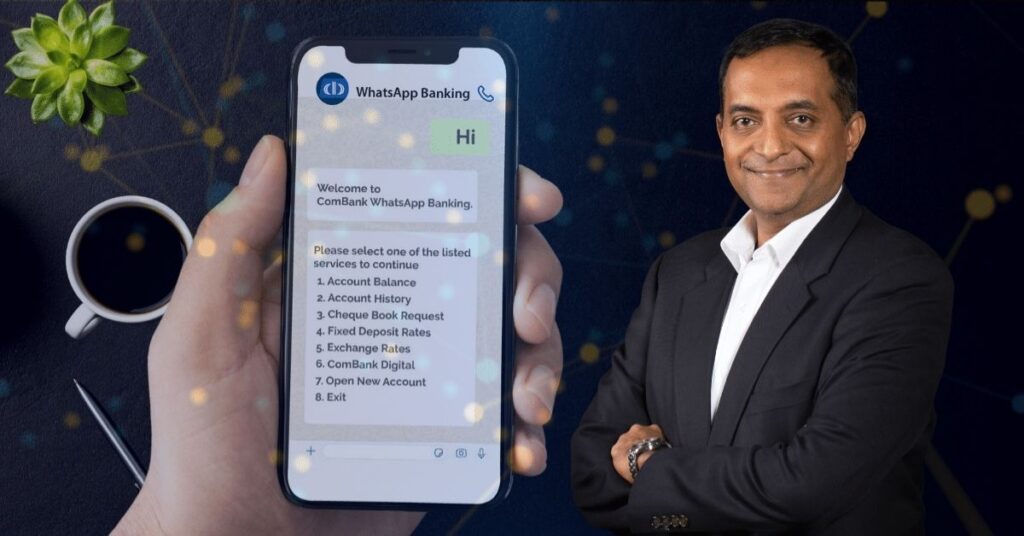

Well done to the hSenid Mobile team powering Commercial Bank’s WhatsApp interface

Back in 2001 hSenid Mobile launched the first SMS banking in Sri Lanka. 20 years later WhatsApp banking is another step by hSenid Mobile to ensure Sri Lanka is on-par with other leading technology nations. hSenid Mobile Solutions has been part of TADHack and TADSummit since the beginning in 2013.

Will private wireless kill network slicing before it even gets started? No.

This is an apples and oranges comparison. Private mobile networks have existed for decades. The WiFi in your office is a private wireless network. If you’re a multi-site organization, you may have those islands interconnected over the internet (best effort) or private circuits (SLA).

However, 5G SA and the availability of open source base stations like FreedomFi; and interest from ‘non-telco’ providers like Dell, have many people excited about 5G private enterprise networks. You need installers that can deploy the stuff, it’s not like WiFi. And it’s still in the fun geeky phase, if you’re not deploying an expensive system from one of the traditional telco vendors. But it’s definitely there and growing.

Network Slicing has been around for 20 years, think of it as a VPN across a telco’s network to all the enterprise’s mobile phones wherever they may be on the network – coverage matters. When NFV (telco-special virtualization) was the fashion, its was assumed that would enable network slicing. Once the fashion moved onto containerization (cloud native), the reality of network slicing across legacy (2-4G) networks became apparent. So the focus is network slicing on 5G SA, as it’s baked in. But adequate 5G SA coverage is a few years away, and people are not upgrading their phones as often, with 3 years being the average, that upgrade cycle will tend towards that of laptops of about 4 years.

I’ve not brought up the security issues in network slices if the enterprise runs their own software, which could lead to malicious VMs or crashing VMs into the hypervisor to then start messing with other VMs. This is not a hold-point, simply an example of the expanded complexity network slicing must manage.

Long story short: private mobile networks have exists for decades and will continue to grow, some will migrate to 5G thanks to the potentially much lower price points, and some new enterprises and service providers will join the private mobile network party thanks to those price points. All this is independent of network slicing.

Network slicing will need adequate 5G SA coverage, and compelling use cases. The usual automotive, transport, healthcare and manufacturing use cases have the challenge that many of the existing solutions are good enough, coupled with the usual host of practical issues when trying to insert a network into principally web/internet services. The success of network slicing is down to the benefits the customers’ experience with network slicing, not private mobile networks. Given network slicing is baked into 5G SA, it’s going to be there, it’s not DOA (Dead on Arrival), rather its adoption is the uncertainty beyond a niche.

People, Gossip, and Frivolous Stuff

Dannel Shanker is now Sales Engineer at Intercom, conversational agent.

Daisy Su is now IoT Product Manager for 5G Automotive at Verizon, after a long stint with Lucent / ALU / Nokia.

Omar Paul is now Principal Product Manager at Amazon Web Services (AWS). We first met when he was VP Product at Shango.

Tim Leidinger is now Channel Sales Manager at Empolis Information Management.

Antón Rodríguez Yuste is now Principal Software Engineer at New Relic, a tool to visualize, analyze and troubleshoot software. He is in this photo from a post made last week by Randy Resnick of TADHack 2015, he’s on the third table from the front on the right hand side.

Amazon’s Private Labels – its complex, but it’s more or less a monopoly

I agree in principle private labels are generally good for the consumer. But the analogy to the department stores belies Amazon’s dominance in being 50% of online sales in 2021. Sears department store peaked at 30% of department store sales, and there was still significant main street / high street competition.

In a department store you can compare branded and own-brand goods physically. Online it’s not that easy, as this article from The Verge on Peak Design shows, the cards are very much skewed in Amazon’s favor.

Coming from the UK, store brands (private labels) are popular and fill a variety of consumer needs. Sometimes it’s cheap and cheerful, sometimes it fills a gap only that retailer can see across its customer base. But there is lots of supermarket competition in the UK – M&S, Tescos, Sainsbury’s, Aldi, Morrisons, Asda. Amazon is almost a monopoly when it comes to online shopping. On the fortnightly recycling day, its Amazon cardboard boxes, not Walmart boxes, stacked next to the recycling bin with the bottles and tins.

I’m as guilty as all my neighbors. Amazon makes it easy. I shop for some clamps, Amazonbasics brand is great value, with great reviews, with one click I buy now and get it tomorrow. I can not buy electric drills at my local hardware store anymore. They can not buy them for what Amazon sells them. I was advised I still had time to order within the next hour on Amazon for same day delivery! But I really needed that drill now….

I think Amazon’s dominance over online shopping and especially the data people have access to to make an informed decision when buying online, mean comparisons to department stores are not quite valid. Amazon should be considered a monopoly at this point, consumers need protection from the outcome of their laziness 😉

Blacc Spot Media, Inc. is celebrating its 10th year anniversary today!

Congratulations to Lantre Barr and the team 🙂 You can see Lantre’s interview at TADSummit EMEA / Americas 2020 here.

You can sign up here to receive the CXTech News and Analysis by email.