The purpose of this CXTech Week 26 2024 newsletter is to highlight, with commentary, some of the news stories in CXTech this week. What is CXTech? The C stands for Connectivity, Communications, Collaboration, Conversation, Customer; X for Experience because that’s what matters; and Tech because the focus is enablers.

You can sign up here to receive the CXTech News and Analysis by email or by my Substack. Please forward this on if you think someone should join the list. And please let me know any CXTech news I should include.

Covered this week:

- Podcast 76: Truth in AI, Consig AI, RJ Burnham

- The End of Telecoms History by William Webb

- Horisen’s Message in Popular!

- RCS Spam

- June 2024 RTC Security Newsletter

- Twilio is Returning to its original SaaS Message.

- People, Gossip, and Frivolous Stuff

Podcast 76: Truth in AI, Consig AI, RJ Burnham

RJ Burnham is the founder / CEO of Consig AI. I’ve known RJ since his time with Voxeo, which spun out Tropo, a competitor to Twilio, that was sold to Cisco. I really like how RJ positions his experience, he’s been working in voice AI for over 25 years. AI being the latest tool to enhance voice communications.

RJ will be presenting at TADSummit 2024 in October, 22-23. His session is:

Voice AI: Breaking Past the Bullshit

RJ Burnham, Founder & CEO at Consig AIWhile AI is the latest buzzword, there’s a lot of hype overshadowing the real advancements. The world of voice AI is evolving at breakneck speed. What was impossible a few years ago is now within reach.

But with these advancements come new challenges. From barge-in issues to streaming models, we need to rethink our approach to harness the full potential of voice AI. Having worked on voice “AI” since the 90s, I’ve seen the technology grow and transform.

This talk dives into the complexities, addresses the current gaps, and explores cutting-edge solutions that are reshaping the industry.Topics will include:

* Rethinking barge-in for seamless interactions;

* Tackling real-time processing and latency; and

* Leveraging streaming models for better performance.

Consig AI is focused on voice automation, for example long form voice survey responses. In building Consig AI, a critical aspect is flexibility given how rapidly Voice AI is developing.

RJ’s positioning of Consig AI is interesting. He’s not chasing after the shiny new ideas, that field is too crowded. He’s also aware that moves by big players like Microsoft, Google, OpenAI can impact his new company’s plans.

Instead, the fundamental issue Consig solves is all the adapters for existing businesses to get Voice AI working, the blocking and tackling. There’s money to be made on all the integrations. This reminds me of the role Jambonz plays in enabling CX (Customer eXperience) companies (e.g. Cognigy) to add voice to their offers. Focused and solving the integration headache.

We then jumped back to RJ’s time with Voxeo and what learning from there he applies today. Here RJ highlights people are a source of many problems faced by businesses, regardless of industry. And underlying those problems is trust. We see that today with SPAM SMS and robocalling, mobile customers do not trust their communication service providers.

RJ links the trust issue to the hallucinations voice AI has today. There’s a battle between RAG (Retrieval-Augmented Generation) and giving the LLM free reign. Often enterprises prefer free reign as the conversation is more natural. We then discuss ways to mitigate the hallucinations, as there is a cost in breaking rules, while that cost can even be a positive in the right context.

I’m really looking forward to RJ’s session at TADSummit, “Voice AI: Breaking Past the Bullshit”.

The End of Telecoms History by William Webb

William has just published his latest book – “The End of Telecoms History” – available on Amazon ( https://www.amazon.co.uk/dp/B0D83Z5FYJ/ ). Below is a summary. The evidence that we have all the telecoms that we need is strong and corroborated in recent days by Ericsson’s downgrading of their mobile growth forecast and the Virgin Media O2 article on “vanity metrics”.

[Summary follows]

Telecoms networks have improved dramatically over the last 150 years. Initially developments were focused on delivering voice calls to homes and then to mobile phones, and then from the 1990s to enabling Internet connectivity. Data capabilities have improved from early 1.2kbit/s modems to networks that can deliver 100Mbits/s or more. And data usage per person has gone from a few Mbytes/s per month to hundreds of Gbytes – nearly a 1 million-fold increase. It is natural to think this progression will continue forever.

But this is not so. Beyond around 10Mbits/s on mobile phones and around 50Mbits/s on fixed broadband, faster data rates make no difference to most. At those speeds there are other constraints such as the Internet servers that limit responsiveness. And our main use – video – only requires 3Mbits/s for high definition. Our use of data is now levelling off, with growth rates already below 20% a year and likely to fall to 0% – a flat level of usage – before the end of the decade.

Those who are well connected, with good home broadband and good mobile coverage – even if it is only 4G – have all the connectivity that they need. We no longer need to strive for faster networks, for more fibre or for the next generation of mobile technology. The journey that started with Morse and Marconi has come to an end. It is the end of history for telecoms.

Of course, users would like all of this for less, and they would like ubiquity, especially in mobile connectivity and this can be delivered with appropriate government targets and regulatory action.

This change from seeking ever-better networks to having all we need has huge consequences. Politicians should stop fixating on the latest “greatest” technology and instead be concerned about delivering ubiquity at the lowest cost. Regulators need to focus less on market forces and assumptions that they will be auctioning spectrum periodically and look instead at regulation focused on improving fixed and mobile coverage. Operators should accept that they are bit pipes and adopt a utility-like strategy and equipment suppliers need to adapt to a market where operators will replace equipment as it becomes obsolete but will not adopt new technology or expand their network. Innovation should focus on cost reduction rather than capacity enhancement.

This book explains why we have reached the end of history and looks at the implications in detail.

[Editor’s Note]

It’s not really the end of telecom history, rather an important goal has been reached. Fixed broadband is 10 years ahead of mobile broadband, they did internet access first, text chat first, video comms first, video streaming first, web 1 and 2 were over fixed networks first. Mobile caught up and the pipes are more or less fat enough. As you can read in OECD.org and Pew Research Center, the conversation moves onto overall population penetration and technology used.

I’ve mentioned before, I’ve had the same broadband pipe to my home for over one decade, FTTH. It’s simply a flat rate subscription that works, even when the power goes out. However, the services I run over that pipe are constantly changing.

No PayTV, that’s streaming video from Netflix, Amazon, YouTube, etc. More security video cameras facing front and back recording content; more podcast traffic, generally uploads to YouTube; more devices. But no need for QoS (Quality of Service), GSMA take note. Fixed leads the way and its not into QoS.

Check out all the TADSummit Innovators, there’s so much going on in programmable communications / telecoms. I have an unending list of innovators doing cool stuff with voice, video, messaging, and more that may or may not be over the PSTN (Public Switched Telephone Network).

That’s the gap, the fixed and mobile networks are fast enough for internet access, its what role telcos play in all the other services running on top? For consumers it’s unclear beyond voice and messaging. Both of those services are plagued by SPAM and robocalling in some countries. These problems must be eradicated, the current shrug of a shoulder and a half-hearted attempt to fix the problem can not be tolerated. People are dying from the cons let in by spam SMS and robocalling.

Horisen’s Message in Popular!

I did a repost of the Horisen Podcast yesterday, the repost has 1k impressions and 600 views in less than 24 hours. Top viewers for the repost being Syniverse, Turk Telecom, Horisen, Twilio, and Sinch.

“>3k Youtube views on the main video and about 1k views across the shorts.

The Linkedin post has 3.3k impressions from 1.8k viewers. Top company viewers: Sinch (1.1%), Twilio (1.1%), Vonage (1.1%), Telesign (1.0%), Syniverse (1.0%). A couple of reposts, but I do not have the stats for them.

It’s clear the messaging monopolies see HORISEN is the right technology at the right time to save people from SMS (and RCS) spam. “

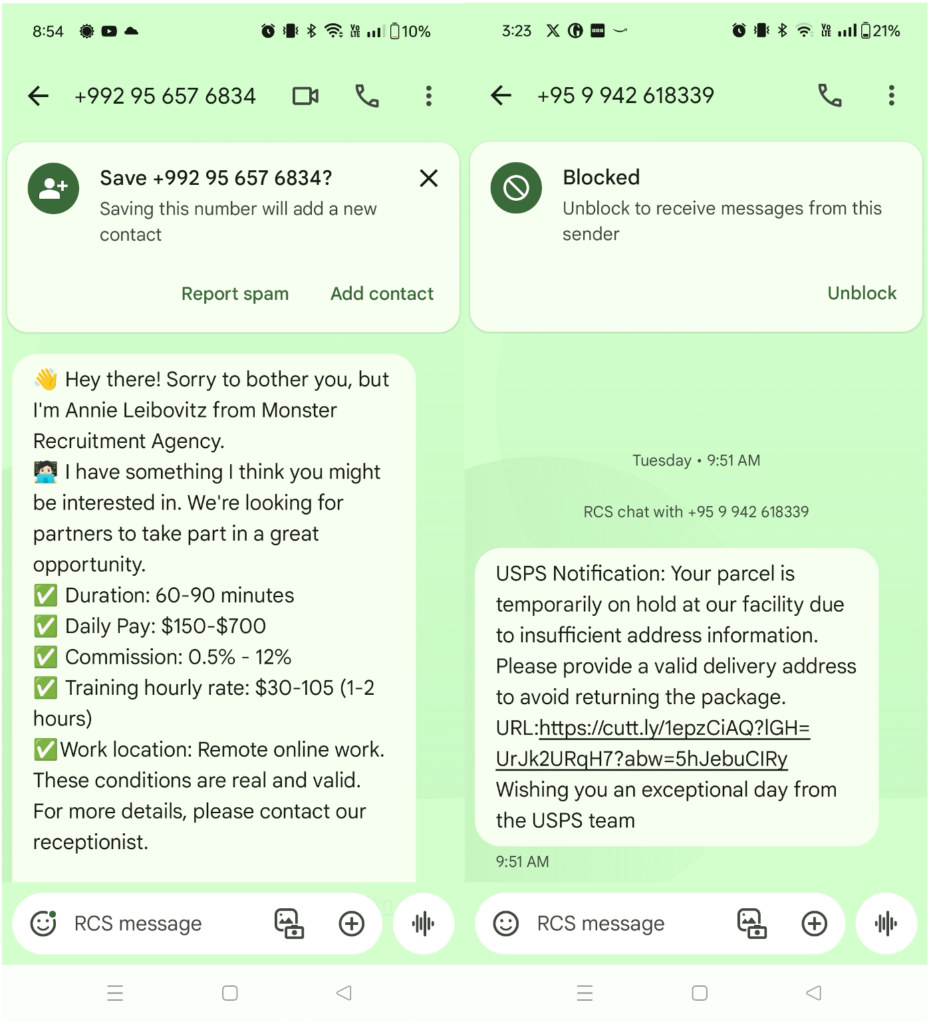

RCS Spam

Received a couple of RCS spam this week. +95 is the country code for Myanmar. And +992 is the country code for Tajikistan. I was having a discussion with Dr. Mustafa Çağrı Sucu on the risks of RCS spam given the ability of it to copy the formatting of web content. This is one to watch!

June 2024 RTC Security Newsletter

Another packed edition with:

- Enable Security’s latest publication on our blog about WebRTC vulnerabilities

- Cisco WebEx’s seemingly obvious vulnerabilities and their effect on military and political entities

- Security fixes in Chrome, affecting WebRTC

- Vulnerabilities in Mitel phones, sngrep, and… iTunes?

- And more!

DoS Vulnerability Affecting WebRTC Media Servers

A critical denial-of-service (DoS) vulnerability has been identified in media servers that process WebRTC’s DTLS-SRTP, specifically in their handling of ClientHello messages. This vulnerability arises from a race condition between ICE and DTLS traffic and can be exploited to disrupt media sessions, compromising the availability of real-time communication services. Mitigations include filtering packets based on ICE-validated IP and port combinations.

This issue has been fixed in Asterisk, FreeSWITCH, and rtpengine. However, Enable Security have discovered it on several well-known public platforms, VoIP services, and proprietary media servers..

Heated Debate on Whether the WebRTC Specs Contain a Vulnerability

Enable Security blog post sparked an engaging discussion on X (formerly Twitter) about whether the vulnerability stems from a lack of security documentation in the RFCs or if it is merely an implementation issue.

Ultimately, even those who strongly believed that this is not a vulnerability in the specs agreed that the specifications may need more explicit guidance on the receiving of media traffic after ICE media consent verification.

Thank you Enable Security!

- Thai Raids Intercept Huge Number of Simboxes and Starlink Satellite Dishes Intended for Scam Call Centers

- The article on Commsrisk is about a major raid in Thailand involving Scam Call Centers. The post includes several images related to the raid with photos of the equipment used, including Telekom SIM cards.

- VoIP relevant quote: “Final leg of communications that also involved a VoIP connection to a scam compound located elsewhere, possibly in another country.”

- News first spotted on Alan Quayle’s newsletter

- TADSummit Podcast Talks About Telco Fraud

Twilio is Returning to its original SaaS Message

Check out this article: https://stocknews.com/news/twlo-infa-smar-3-high-growth-saas-stocks-to-buy-now/

Before 2021 Twilio could lay claim to the SaaS message, it did not get involved in those difficult SMS aggregation deals.

However, after the ‘investment’ in Syniverse of $750M (2022) and the acquisition of Zipwhip for $850M (2021), Twilio solidly positioned itself in the SMS aggregation business, becoming less of a SaaS play. Part of the driver was the price increases in A2P SMS coming from the carriers. Today, Twilio has become an effective A2P SMS monopoly for North America. I should really write Twilio/Syniverse given their ‘close cooperation’. Twilio is a co-owner, along with The Carlyle Group, of Syniverse.

We’ve seen earlier this year the SMS gateway deal it cut with international aggregator, e.g. tyntec, for routes into Mexico and Peru. Twilo is playing a different game internationally, but with a similar end result in dominating routes. https://blog.tadsummit.com/2024/04/01/tyntec-frenzy/

Twilio’s stock ‘seems’ to have settled at around $55-$57 for the time being. In the US we’ve seen Twilio making life difficult for #CSPs (Campaign Service Providers), particularly in toll-free #A2P SMS, since the start of the year. And migrating some CSPs off Zipwhip (because it is closing?) and onto Syniverse. CSPs are reporting the Syniverse platform is less performant than Zipwhip.

The A2P SMS business has become much more tough in North America.

TADSummit is the only place were you’ll have a open and honest discussion on the challenges in A2P SMS, what is really happening. For example, will Syniverse close down the unsanctioned A2P SMS path for everyone in Dec 2024? Is Zipwhip really closed down for Toll Free A2P SMS, is Syniverse the only choice? If you want to send A2P MMS, Syniverse is the only game in town for the US. Given the turmoil in 2024, what is going to happen in 2025! The A2P deals being cut across the industry are not open and fair, in the limit CSPs and brands must sue for their survival, the Federal Communications Commission must regulate, beyond the ‘lightly notice’ suggested by the Von Coalition. https://alanquayle.com/2024/05/von-coalition-proposal-to-fcc/

TADSummit 2024 website is launched:

– registration will be opening soon.

– read more on what we have planned here: https://alanquayle.com/2024/05/tadsummit-tadhack-global-2024/. The agenda is coming together nicely, see Consig.ai podcast above.

People, Gossip, and Frivolous Stuff

Steve (Stavros) Lazaridis is now CTO & President at Phonism. They’ve brought in a CEO to help the company grow.

Suzy Barros Batista is now Senior Executive Business Partner Manager at fabric. I’ve known Suzy through her time at Rogers.

Hadi Hazim is now Head of Business Value Services – GCC Apps at Oracle. I’ve known Hadi for over one decade, since his time at du.

Francisco Maroto is now IoT Sales & Business Development Executive at SEIDOR. I’ve known Francisco for well over one decade, all the way back to his Microsoft days.

Ruben Echarri is now a Solutions Architect at _VIOS. I’ve known Ruben through out his time at Vodafone. _VOIS (Vodafone Intelligent Solutions) is a strategic arm of Vodafone.

Mark Pinnes is now Senior Vice President at Machani Group. We first met during his time at Truphone.

Hugo Lessen is Program Manager Digitally Secure Equipment – IOT. I’ve known him since his time at KPN.

You can sign up here to receive the CXTech News and Analysis by email or by my Substack.